The Difference Between a Contractor and an Employee

The difference between a contractor and an employee differs based on a few basic criteria. The designation is important when determining who pays payroll taxes.

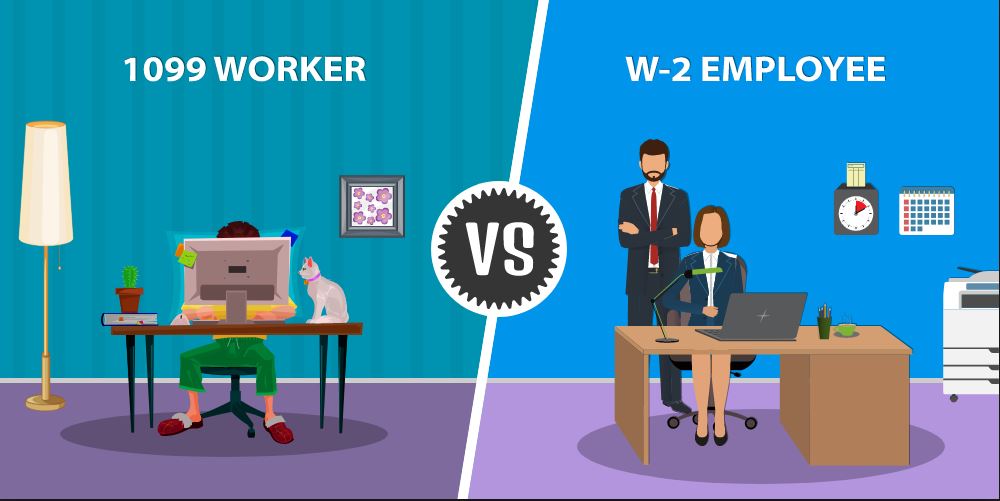

A contractor can name their price to a company in any manner that he or she chooses. A contractor does not receive any benefits that a company would normally pay to its employees, and is not paid any overtime. Compensation may be on an hourly basis, or as a fixed fee in exchange for a predetermined trade or value; thus, the type of compensation is not the determining factor when deciding whether a person is a contractor.

A contractor is paid through the accounts payable system, rather than through payroll. This means that the company is responsible for issuing a Form 1099 to the contractor immediately following the end of the calendar year, which states the total amount paid to the contractor during the calendar year. The contractor (not the company) is responsible for paying all payroll taxes to the government.

A person is an employee if the company controls not only the person’s work output, but also the manner in which the work is performed. The IRS uses the following three criteria to establish whether someone is an employee:

• Behavioral. The company has the right to control how a person does his job.

• Financial. The company controls the business aspects of the person’s job, such as providing compensation and reimbursing for expenses.

• Relationship. The company provides benefits to the person, or there is evidence of a similar situation that appears to indicate a long-term relationship.

There is no single test item that clearly shows a person to be an employee or a contractor. Rather, you should make the decision based on the total of all the above factors. If you are still uncertain, feel free to contact your CPA firm to help you decide.

An employee is paid through the payroll system, which means that the company employing the person is responsible for the company’s portion of any payroll taxes, for unemployment insurance, for withholding any applicable taxes from employee paychecks, and for remitting all taxes to the government.

There is a tendency for companies to classify as many people as possible as contractors, so that the companies are not liable for payroll taxes. However, if the government concludes that a company should have defined someone as an employee, then the company is still liable for these taxes after the fact. Thus, if there is not a clear case for treating a person one way or the other, it is generally safer to classify the person as an employee than as a contractor.